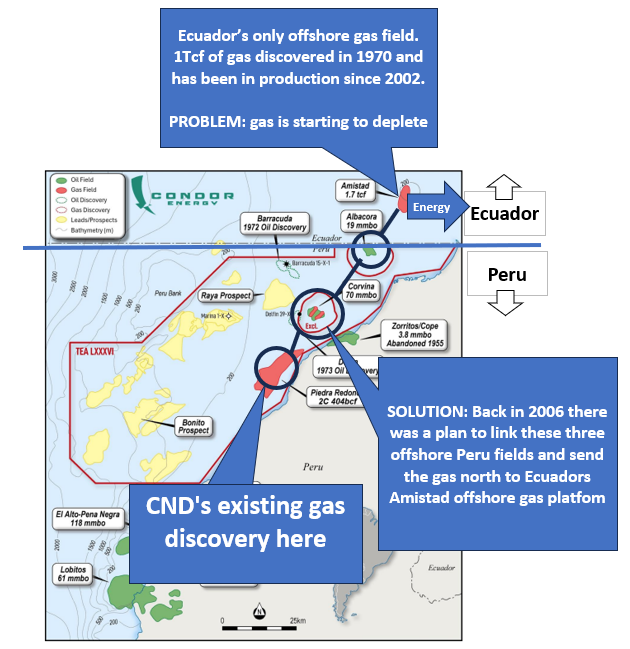

CND completes commercialisation study for 1 trillion cubic feet gas discovery

Our 2023 Pick of The Year Condor Energy (ASX: CND) just announced the results of an “independent market and commercialisation study” for its 1Tcf gas discovery.

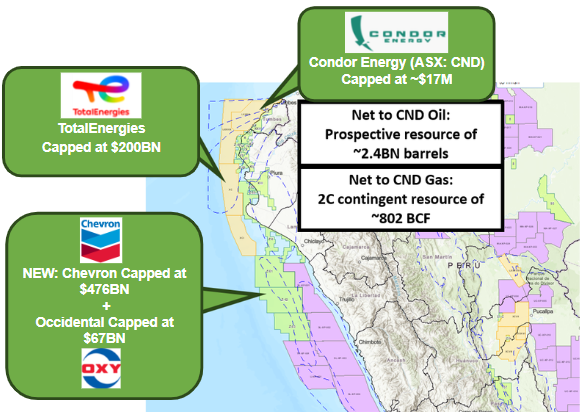

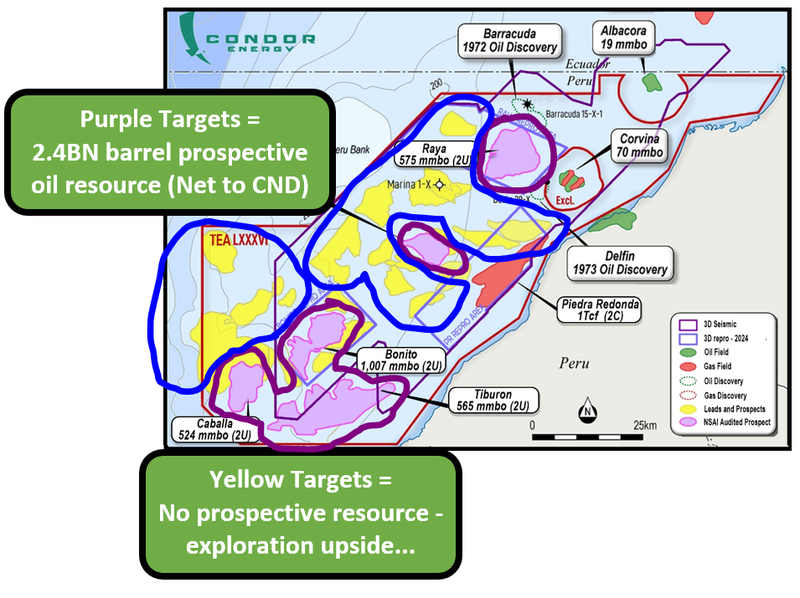

CND holds 80% of a big oil and gas block, offshore in Peru.

CND’s block is surrounded by $200BN Total Energies and more recently $476BN Chevron and $67BN Occidental have picked up blocks in offshore Peru.

CND’s project currently has:

- A 1 Trillion Cubic Feet (Tcf) discovered gas field, AND

- ~3BN barrels of undrilled prospective oil resources

Today’s study solely relates to CND’s gas discovery and at a very high level it lays out the case for what can be done with the discovery - i.e how CND (or any other operator interested in the asset could develop it).

Here were some of our key takeaways from today’s announcement:

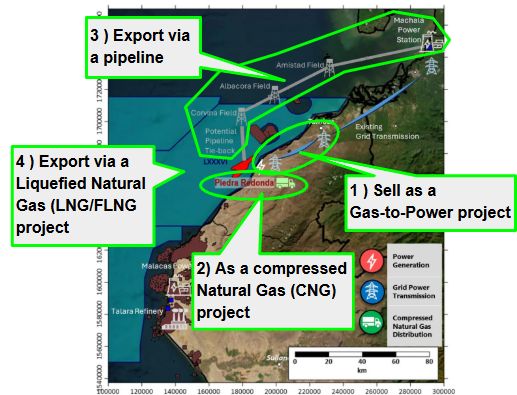

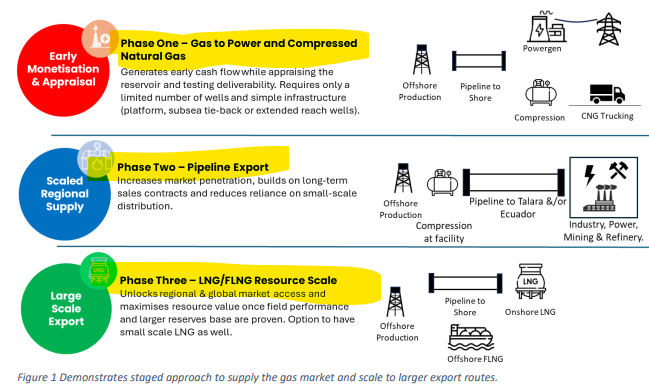

The asset could be developed in four ways

The study laid out four different commercialisation scenarios for the project.

Including:

- Sell as a Gas-to-Power project - this would be where the gas is delivered to local demand centres in Northern Peru. Northern Peru has limited gas supply with strong and growing demand in industrial, mining, and residential sectors.

- As a compressed Natural Gas (CNG) project - this would basically require the building of a CNG facility so that the gas can be shipped to regional markets and within Peru.

- Export via a pipeline - the development scenario would be by delivering the gas to the Talara refinery, industrial users or north to Ecuador. Ecuador actually faces electricity shortages so CND could tie in via the underutilised Amistad gas field and Machala Power Station.

- Export via a Liquefied Natural Gas (LNG/FLNG project - this would be the longer term export scenario where gas from the field could be sold internationally.

(Source)

CND’s project is big enough to be developed in stages

The study also underscored the size of CND’s gas field.

Because of the 1 Tcf resource, there is potential to develop the project in stages using a combination of the above options.

The scenario laid out in the study was to start small and deliver gas regionally to get the project into production, then start building out pipeline/LNG infrastructure to connect the project to markets outside of Peru:

(Source)

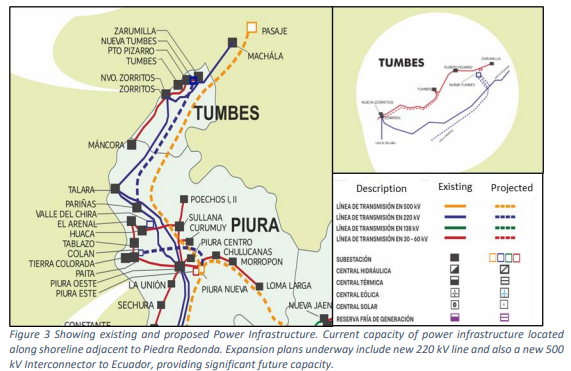

There is existing infrastructure in the region

The study also outlined all of the infrastructure that could benefit CND’s project and make development a lot lower cost than it would have been otherwise.

CND’s project is only ~4-10km away from the coast in shallow water which would make development a lot easier than if it were in deep water.

The project also has direct power grid access - the Tumbes currently has ~150MW of installed capacity and is linked to Ecuador by a 110MW interconnector.

There is also expansions planned for this infrastructure with a new 220 kV line in northern Peru and a 500 kV Peru–Ecuador interconnector.

(Source)

Overall we think the study lays out the case for how CND’s gas project could be developed really well and as mentioned in today’s announcement we would expect it to help with partnering discussions.

(especially because its an independent study).

(Source)

Next major catalyst we want to see is a deal…

CND has explicitly said before that it had commenced a “Farmout process” on its block “with multiple parties in (the) data room”.

CND picked up its project ~24 months ago and has spent most of that time reprocessing 3D seismic data, and putting together a portfolio of drill targets.

CND is now at the stage where it is ready to either go down the route of drilling one of its targets OR bringing in a partner to fund whatever drilling/development plan the company has.

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND deals out its gas asset - maybe some of the proceeds that come from this can go toward drilling an exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe?

- CND deals out oil exploration assets - CND gets a free carried interest in a well that would be fully funded by a farm-in partner. This means less dilution going into a big drilling event for existing shareholders…

- Maybe a combination of the two? - CND could bring someone in that is interested in both…

As mentioned earlier, Occidental, Total and Chevron are active in the region and there have been some big deals done on assets in this part of the world before.

Back in 2009, KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND’s block.

(Source)

We like that CND has two parts of its project it can deal out and with a current market cap at $17.9M we think CND is leveraged to a big drilling event OR a deal that sets the basis for developing its gas asset.

The two key reasons why we think CND is “deal ready”

We covered the two key reasons in detail in our last CND note, here is a quick overview (click on the hyperlinks to see our deep dive on the two reasons):

1. We think the oil prospects are big enough to warrant drilling AND IF someone gets lucky and discovers something there are plenty of other leads that can be followed up over CND’s blocks.

2. Because a development scenario was considered for the gas asset back in 2006. Now with more demand for gas locally (in both Peru and Ecuador) as well as internationally, we think the chances someone relooks at that old development plan is much higher...